Ways to Finance a Cabin or Lake Home

Traditional Mortgage Loan: Just like financing a primary residence, you can apply for a traditional mortgage loan through a bank or mortgage lender. This option typically requires a down payment (often ranging from 10% to 20% of the purchase price) and involves paying off the loan over a fixed term, such as 15 or 30 years. The interest rates and terms will depend on your creditworthiness and the lender's policies.

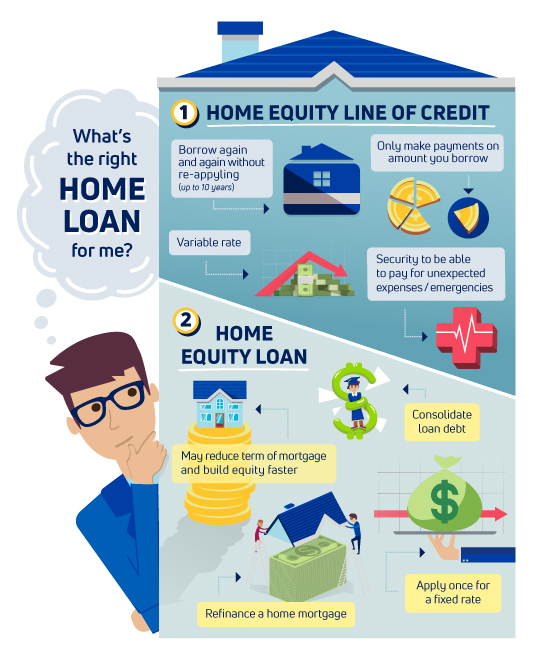

Home Equity Loan or Line of Credit: If you already own a primary residence with built-up equity, you can consider tapping into that equity through a home equity loan or line of credit. These options allow you to borrow against the value of your primary home to finance the cabin or lake home. The interest rates and terms may be favorable, but it's important to carefully consider the risks and ensure you can handle the additional debt.

Cash-Out Refinancing: If you have equity in your primary residence, you can refinance your existing mortgage and take out additional funds to finance the cabin or lake home. This option allows you to replace your current mortgage with a new one that has a higher loan amount. The interest rates and terms will depend on current market rates and your financial situation.

Owner Financing: In some cases, the seller of the cabin or lake home may be open to providing owner financing. This means that instead of obtaining a loan from a traditional lender, you make payments directly to the seller over a specified period. The terms and interest rates are negotiated between the buyer and the seller, and a formal agreement is typically drafted to outline the terms of the financing arrangement.

Personal Loan: If the cost of the cabin or lake home is relatively low, you may consider taking out a personal loan from a bank or online lender. Personal loans typically have shorter terms and higher interest rates compared to mortgage loans, but they may offer flexibility in terms of repayment and can be secured relatively quickly.

Vacation Home Loan: Some lenders offer specific loan programs for vacation homes or second homes, including cabins or lake homes. These loans may have slightly different terms and requirements compared to traditional mortgage loans, so it's worth exploring this option and comparing it to other financing options available to you.

Regardless of the financing option you choose, it's important to thoroughly research and compare different lenders, loan terms, and interest rates. Consider consulting with a mortgage broker or financial advisor who can provide guidance and help you find the best financing option for your specific needs and financial circumstances.

Comments

Post a Comment